Back in 2016, Dirk Paessler wrote an article in Today’s CIO outlining the progression of Software Defined Networking (SDN), making the point that although a compelling proposition, business couldn’t see a way of adopting the technology which wasn’t expensive, disruptive and risky due to the all-or-nothing implementation model. These challenges created a ‘wait and see’ tone in the market. A year on we are revisiting the SDN market to look at what organisations are doing now, and if they have overcome some of the earlier barriers to adoption. As a quick recap, SDN enables network administrators to manage network services by decoupling the control plane (where the network is traffic going) from the data plane (the underlying systems that forward the traffic on). It is the SDN controller that provides some of the largest strategic gains and the following key benefits:

A single point of control where information security policies and regulations can be distributed across the infrastructure

Real time visibility of network activity

Automated policies which produce dynamic responses to changing utilisation and performance requirements

Cost savings delivered by consolidating traditional multi-point based solutions into a single solution, reducing hardware and operational management costs

Over the course of the past year the market has intuitively peeled back the layers of the SDN proposition, and what has emerged are three common threads, each with typical use cases as illustrated in the following table.

Security

Automation

Application Continuity

Micro-Segmentation

IT automating IT

Disaster Recovery

DMZ Anywhere

Developer Cloud

Metro Pooling

Secure End User

Multi-tenant Infrastructure

Hybrid Cloud Networking

This has allowed businesses to reassess their needs and the benefits of SDN in a much more granular fashion resulting in a significant upswing in discussion followed by tangible market adoption. The total number of organisations across the market who have implemented SDN to any degree is only just progressing past the early adopter phase but there is now enough critical mass forming the early signs of ‘popular wins’. Organisations are seeing results in the following areas:

Network provisioning reduced from days to minutes in some cases

Choice over a library of logical networking elements and services, such as logical distributed switches, routers, firewalls, load balancers, and so on

Operational efficiency gains through SDN automation and network segmentation

Improved integration of existing third party network and security solutions

Further maturity gains in conjunction with the IT-as-a-Service (ITaaS) consumption model with cloud management integration and self-service

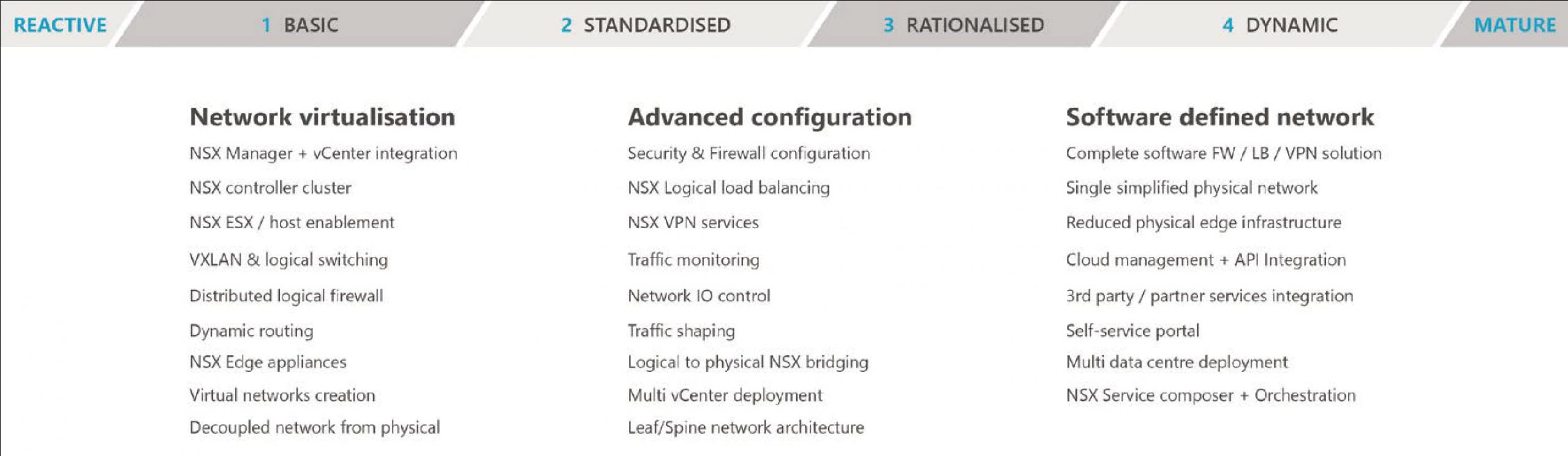

Some of the challenges that had been identified in 2016 do still exist. Critically, organisations being able to measure and realise benefits of SDN adoption still depend on them fully understanding their business and technical objectives. An approach to address this is to align business requirements and maturity against tiers of granular functionality and complexity. In simplistic terms, the more mature the organisation, as defined by whichever ITSM model you prefer to use, the greater the likelihood of IT being ready or successful in adopting the more complex or disruptive functions of SDN. In the context of VMware’s NSX software-defined networking technology, the following diagram illustrates this viewpoint as a mapping between an ITSM maturity curve and some selected SDN scenarios. As industry advisors, over the past year we’ve subsequently worked with many organisations within finance, education and healthcare, demonstrating that this more granular approach to aligning technical capability against use cases will lead to successful implementations. The following table helps to tangibly highlight some of these success stories.

Global Use Case

Use Case Description

Specific Requirements

Customer Edge Demarcation

Virtualisation of the customer edge through virtualised platforms on top of a physical network presence. Typically for multi-tenant offerings spanning complex infrastructure. Objectives are achieved by moving functions closer to the core of the virtualised infrastructure

On Premise vCE

Hosted vCE

Network Virtualisation

Deliver a management layer through software to control the physical environment. Meets a need to deliver fine or specific controls and isolation across multiple racks or locations. Inserts isolation through security and accelerates service delivery.

Campus/Organisation Virtual Networks

DC Micro Segmentation (Test/Dev or Operations and Development

DC Virtual Networks

Network-as-a-Service

Dynamic Interconnects

Meets a requirement to dynamically link locations (DC’s, Public or Private Infrastructure). Adhere to SLAs for QoS levels on the links

Cloud Bursting

Virtual Private Networks

Dynamic VPN

Cross Domain management

Optimising Multi-Layer traffic

Virtualised Aggregation of Core Infrastructure

Organisations who want to virtualise core systems (i.e. service providers) including support infrastructure

Mobile Network Virtualisation

vPE

GiLAN

vEPC & vIMS

Datacentre Optimisation

Optimise networks to improve infrastructure or application performance, automate and orchestrate workloads with networking configuration

Big Data Optimisation

Workload Optimisation

Network Access Control (NAC)

Specific privileges for users or devices accessing a network, including limiting access controls.

Unified Communications

Remote/Branch NAC

Campus NAC

Source: Sdxcentral So, in answer to the question, have we moved on from the tentativeness of 2016? The answer is a definitive yes. The maturity within the market has and continues to improve, organisations are getting to grips with what SDN means to them through a more granular approach, and are being selective about their entry points to SDN. The successful ones are applying managed maturity processes aligning technical capability to corporate objectives, thereby banking solid incremental strategic gains, and delivering organisations real value. Has the market ultimately surprised us? Certainly the rapid adaptation has been fascinating to see unfold and mature. However as always, no matter how a good solution is, success lies in the planning and execution!

In the context of VMware’s NSX software-defined networking technology, the following diagram illustrates this viewpoint as a mapping between an ITSM maturity curve and some selected SDN scenarios. As industry advisors, over the past year we’ve subsequently worked with many organisations within finance, education and healthcare, demonstrating that this more granular approach to aligning technical capability against use cases will lead to successful implementations. The following table helps to tangibly highlight some of these success stories.

In the context of VMware’s NSX software-defined networking technology, the following diagram illustrates this viewpoint as a mapping between an ITSM maturity curve and some selected SDN scenarios. As industry advisors, over the past year we’ve subsequently worked with many organisations within finance, education and healthcare, demonstrating that this more granular approach to aligning technical capability against use cases will lead to successful implementations. The following table helps to tangibly highlight some of these success stories.  In the context of VMware’s NSX software-defined networking technology, the following diagram illustrates this viewpoint as a mapping between an ITSM maturity curve and some selected SDN scenarios. As industry advisors, over the past year we’ve subsequently worked with many organisations within finance, education and healthcare, demonstrating that this more granular approach to aligning technical capability against use cases will lead to successful implementations. The following table helps to tangibly highlight some of these success stories.

In the context of VMware’s NSX software-defined networking technology, the following diagram illustrates this viewpoint as a mapping between an ITSM maturity curve and some selected SDN scenarios. As industry advisors, over the past year we’ve subsequently worked with many organisations within finance, education and healthcare, demonstrating that this more granular approach to aligning technical capability against use cases will lead to successful implementations. The following table helps to tangibly highlight some of these success stories.